The European Edtech Funding Report 2022

- The Brighteye Team

- Jan 27, 2022

- 8 min read

Updated: Oct 2, 2022

Welcome to the Third Edition of the European Edtech Funding Report!

In Edtech circles, 2020 will of course be remembered for the tumultuous experiences of those in the education sector, with schools, universities and workplaces closed to slow the spread of the virus. It will also be remembered as the year that the sector woke up to the solutions being developed by Edtech companies to help people learn faster, more affordably, more efficiently and more effectively.

It is no surprise, then, that 2021 saw a boom 💥 in Edtech investment from across the spectra of investors, from governments to VCs to institutional investors, including generalists- these organisations developed conviction that the sector is capable of producing the same kind of outsized returns generated in fintech, healthtech and other sectors better recognised for their growth. 📈

At Brighteye, we are excited about this new era for Edtech and determined to help Europe lead the way. With dramatically reduced barriers to customer, we see a prosperous trajectory for impact investments, and the ever-growing interest of US investors in European markets, we see a prosperous trajectory for entrepreneurs and founding teams operating in the space. 💸

This report takes a deep dive into venture funding in the last 12 months across global and European Edtech, including both historical and global data sets to provide broader context. For the first time, thanks to the team at Dealroom, we include data on founder gender distribution.

Within this post we will focus on European Edtech funding, contextualised with headline global data. We dive into more detail in the full report, which you can access below:

Methodology

In recent months, we have been working closely with Dealroom to develop the leading open-sourced Edtech-focused data platform. In this report, we have used Dealroom’s data as a starting point and where appropriate, consolidated it with relevant insights from Crunchbase, Pitchbook, Tracxn and our previous work.

We would like to thank Dealroom for their co-operation in the production of this report. 🙏

Global context:

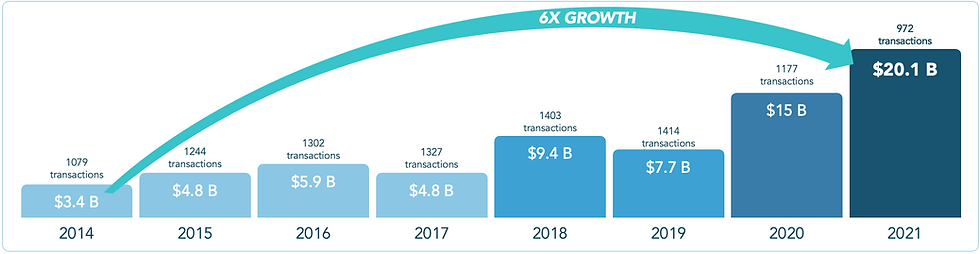

1. Global Edtech VC funding in 2020-2021 equals funding during the entire 2014-2019 period

The step-change in VC funding since 2019 is clear to see- funding doubled between 2019 and 2020 and continued rising in 2021 with 34% further growth in global Edtech funding. The combined funding figures for the two-year period of 2020-2021 equal funding secured during the entire six-year period of 2014-2019, reflecting the fact that a growing number of edtech companies demonstrated the dynamism and growth needed to raise large rounds.

Increasing funding is one measure of vibrancy in the ecosystem – however, the other major indicator of ecosystem vibrancy is deal count. Deal count has fluctuated quite considerably since 2014 – interestingly, the total in 2014 of 1079 is higher than the total in 2021 of 972, following a peak in deal count in 2019 of 1,414 (the 2021 total is 69% of the 2019 figure). It appears that lower deal count follows higher VC funding totals, as the ecosystem matures, proven winners absorb more capital and angel investors’ involvement in Edtech increases.

2. Edtech VC investment in China hit a wall, while US and Europe took flight

Edtech VC funding to companies based in the US in 2021 has jumped to 46% of the global funding total ($9.3B), from 22% ($3.3B) in 2020. This represents a significant shift in the dominant region by VC funding- in 2020, China saw 54% ($8.1B) of global Edtech VC, compared to 9% ($1.9B) in 2021. Political factors contributed to the stall in Edtechinvestment in China in 2021(1), highlighting broader regulatory risks in the Chinese tech sector. A stalling Chinese Edtech scene, combined with a booming European market saw Edtech VC funding in Europe exceed the level in China for the first time, a great landmark, though still 27% of the amount being invested in the US. This said, the trend of diversification of funding across global regions appears here to stay, evidenced by the leap in funding seen in regions labelled ‘Rest of Asia’ with India an increasingly advanced Edtech hub (India secured $4.0B in VC investments in 2021), and ‘Rest of World’ with Australia seeing the minting of its first Edtech unicorn (Go1).

Tom Singlehurst, Global Head of Education Research at CitiBank observes that “the change in the regulatory landscape in China has resulted in a shift of focus for public market investors in two directions. First, we have seen a shift from East to West, with much more focus on Western Europe and US/ Latam opportunities. Second, we have seen a corresponding shift from K-12 to adult/professional learning. It is interesting to see a similar phenomenon in VC funding.”

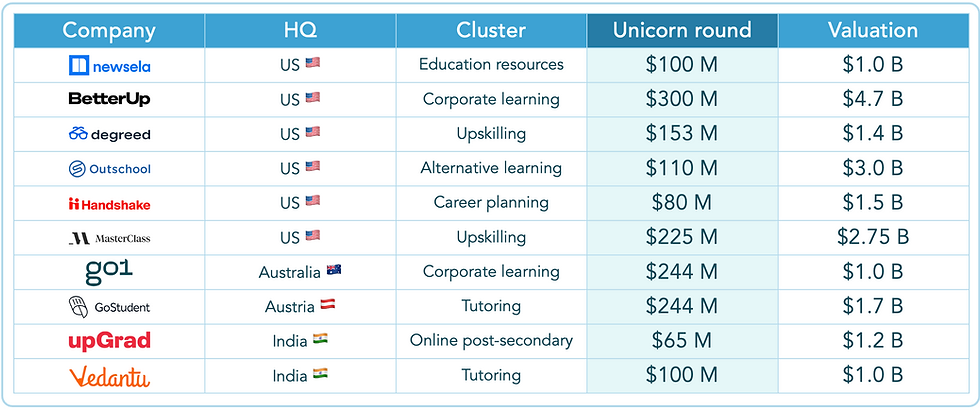

3. More than 1/3 (23) of all Edtech unicorns ever were minted in 2021

As of early January 2021, there were 32 pre-exit Edtech unicorns around the world that have collectively raised more than $27B in funding- the list of 32 companies excludes companies like Udemy (IPO, October 2021) and Duolingo (IPO, July 2021). There have been 64 unicorns, the first of which was minted in 2014. 23 Edtech companies became unicorns in 2021 and 81% of unicorn rounds were over $100M.

Valuations were, on average, 13X the size of the round- Go1 had the lowest valuation relative to the size of its round (4X), while Outschool had the highest valuation relative to the size of its round (27X). We have termed this ‘dilution per round’, reflecting the multiple between the size of the round and the valuation. Within the selected companies selected above, the average funding round in which companies reach unicorn status is Series D.

The most common areas in which Edtech unicorns appear to be minted include corporate learning (BetterUp and Go1), tutoring (GoStudent and Vedantu) and upskilling (MasterClass and Degreed). although companies selling into schools (Newsela) and universities (Handshake) have also reached unicorn status. There is also increasing diversity in the home markets of these unicorns- with GoStudentbecoming Europe’s first Edtech unicorn (when excluding Kahoot! as it’s listed) and Go1 becoming Oceania’s first Edtech unicorn.

Spotlight on Europe:

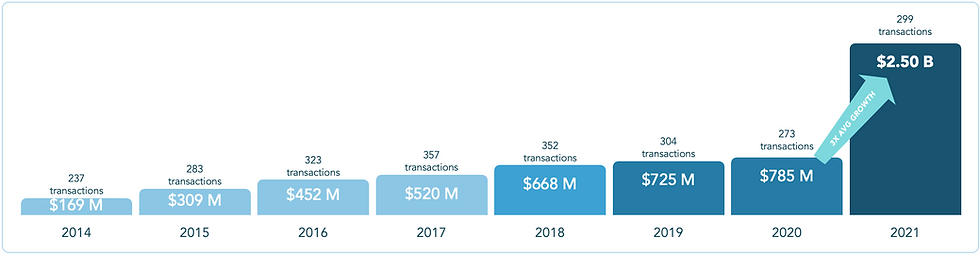

4. European Edtech VC increased by >3X, breaching $2.5B by year-end

As Brighteye reported throughout 2021, European Edtech VC investment was on course from early in the year to more than double, having first passed the $1B mark in a calendar year in July. European Edtech VC investment continued to accelerate through the end of the year, breaching $2.5B in December 2021. This represents a coming of age for European Edtech, finally receiving VC investment on a scale more competitive with regions further along in their development, as highlighted in the initial charts. The growth in VC investment between 2020 and 2021 has been nothing short of explosive. It took a year for the shocks of the pandemic to reverberate through to VC investment in the region, as understanding of new verticals, early leaders and possible returns crystallised.

The number of Edtech deals in Europe follows a similar trend to the global figures, having risen steadily between 2014 and 2017, before a steady fall between 2017 and 2020, rising again to 299 in 2021. This is positive, but growth in deal count has not been explosive in the same way as total VC funding- it represents the steady and hopefully sustained expansion of the sector in Europe.

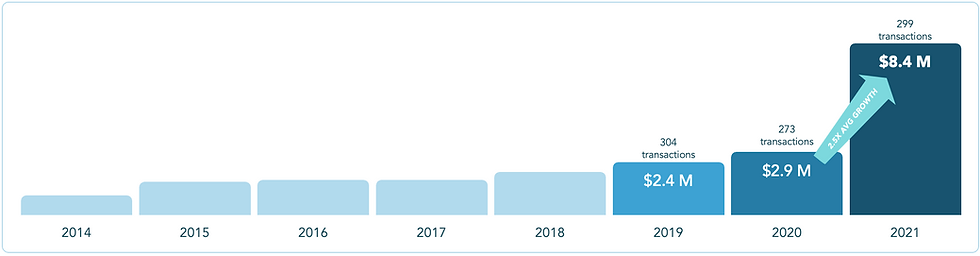

5. Average deal size in Europe has increased significantly, nearly tripling from $2.9M in 2020 to $8.4M in 2021

Average deal size in Europe has followed a similar trend to the global figures, though at a lower starting point. Average deal size has risen steadily from $0.71M in 2014 to $2.9M in 2020. This leapt up in 2021 to $8.4M, representing 3X growth from 2020, driven partially by faster growth of Edtech companies and higher valuations. This represents growing maturity in the sector. It also reflects deal count hasn’t jumped massively, despite the significant increases we have observed.

6. The portion of global Edtech deals done in Europe is increasing

Since 2019, the portion of global Edtech deals done in Europe has risen 10% in 2 years, from 21% in 2019 to 31% in 2021, even as the pie itself got bigger. This highlights the increasing health of the European ecosystem, across all round sizes and sub-industries as well as investors’ growing realisation that enormously successful companies can be spawned in the region.

7. A broadening mix of generalist & specialists VCs in European Edtech

For the second year running, Brighteye Ventures has been the most active fund in Europe by number of Edtech deals.

While the gaps between the number of deals completed by specialists and generalists has maintained, the number of deals completed by generalist funds with an interest in Edtech has increased- e.g. Softbank (9), Global Founders Capital (8) and Vershina Capital (6). Most Edtech specialists, like Brighteye Ventures, tend to focus on early-stage deals (at Pre-seed, Seed and Series A), while generalists with increasing interest in Edtech tend to be focused on later stages (Series B onwards), crudely explaining involvement in fewer, larger deals.

Tom Singlehurst, Global Head of Education Research at Citi, commented that the ”increasing interest in Edtech as a significant opportunity for VCs mirrors growing interest in education from public market investors. This interest incorporates not only an appetite for an area which exhibits strong underlying growth on the back of digitisation/technology adoption but also, importantly, a growing need for public market investors to find areas where their capital can also effect broader societal change. Edtech fits the bill on both counts.”

8. The sector is maturing, with an increasing portion of high-value deals

In perhaps the clearest indication of the European ecosystem’s maturity, while the number of deals has been increasing, there are a growing portion of high-value deals being struck, as companies both raise larger, early rounds and move through funding rounds as they progress. For example, 70% of deals in 2017 were of less than $1M, but this has shrunk to 40% in 2021. The remaining 60% in 2021 represents deals of more than $1m, with 33% of $1-4m, 15% of $4-15M, 7% of $15-40M, 5% of $40-100M and 1.1% of $100m+.

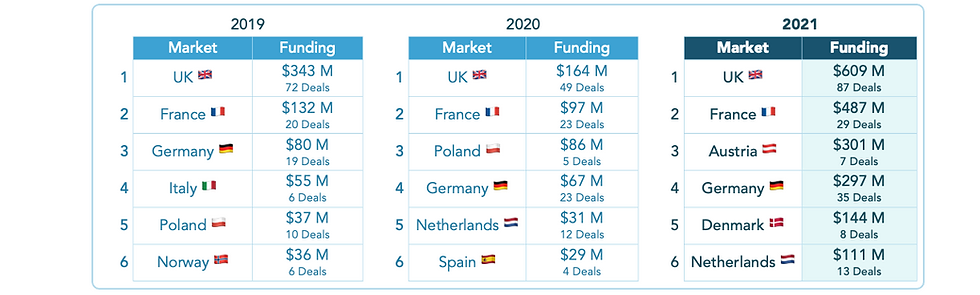

9. The European landscape is broadening- 6 markets received >$100M in 2021, compared to 1 in 2020

VC funding in European Edtech is spreading across the continent- the Edtech ecosystem is no longer a small pond, getting deeper, with the UK and France dominating the top two by total funding, but a large, deepening lake lake, with funding heading to a far broader set of markets.

Before 2021, only two markets had exceeded $100M in Edtech VC investment in a single year (UK and France), but in 2021, this became 6 markets (UK, Austria, France, Germany, Denmark and the Netherlands). The UK aside, exceeding $100M in investment was driven by 1 or 2 larger deals exceeding $50m. For instance, $275M of Austria’s Edtech VC investment of $301M (91%) was secured by a single company, GoStudent. Similarly in Denmark, $115M of $144M was secured by two companies, Eloomi ($55M) and Labster ($60M). This skews the average deal size in these markets (Austria- $43M; Denmark- $18M; UK- $7M; France- $17M).

Totals aside, the UK dominated deal count, with 87 of Europe’s 299 deals (29%). This is more than 2X the deal count of any other European market, with France and Germany seeing 29 and 35 deals respectively.

10. In Europe, male founding teams raised 27X more than female founding teams, across 6X as many deals

In the European context, 80% of 2021 Edtech VC investment was secured by male founding teams, compared to 3% for female founding teams and 17% for mixed founding teams. The ratio of funding received (using non-rounded numbers) by male founding teams compared to female founding teams is 27:1. This is partially a reflection of the number of deals struck by founders of each gender (213 deals secured by male founding teams compared to 35 deals secured by female founding teams). This ratio is 6:1.

The average European female founding team is securing $1.8M in investment compared to their average male colleague securing $9.4M, and mixed founding teams raising $8.3M on average. As highlighted in the global data, female founding teams appear to be more common in the early-stage rounds- we hope that as female-led teams progress through the rounds, funding will begin the long path to equalising.

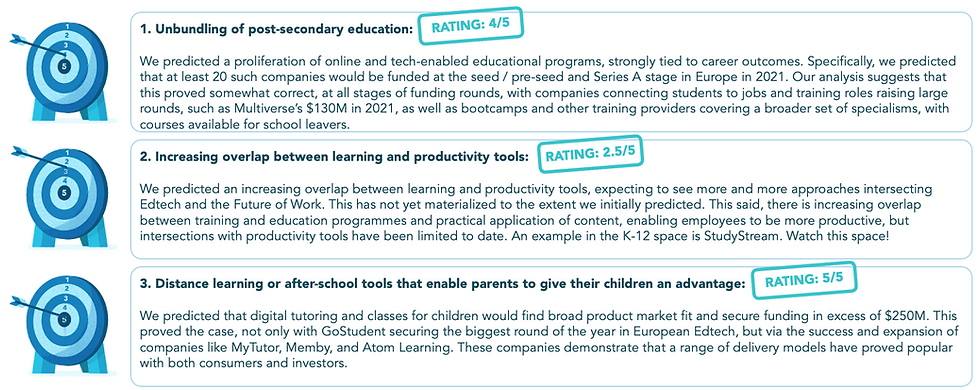

Reviewing our predictions for 2021:

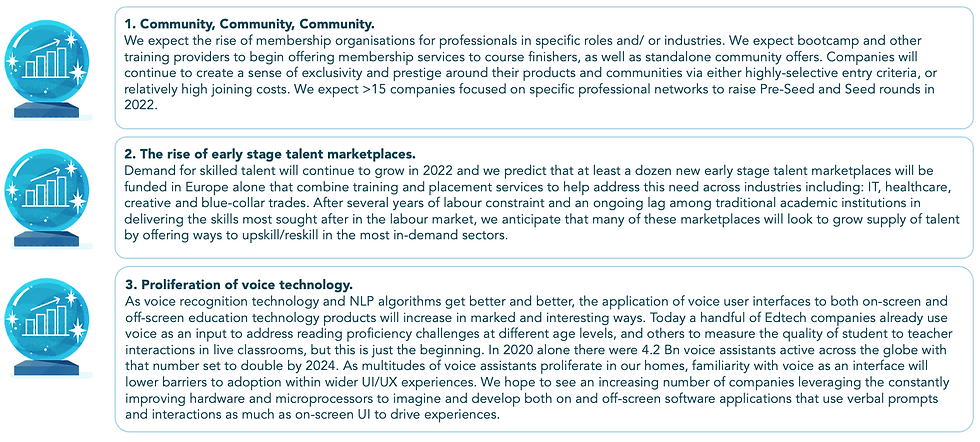

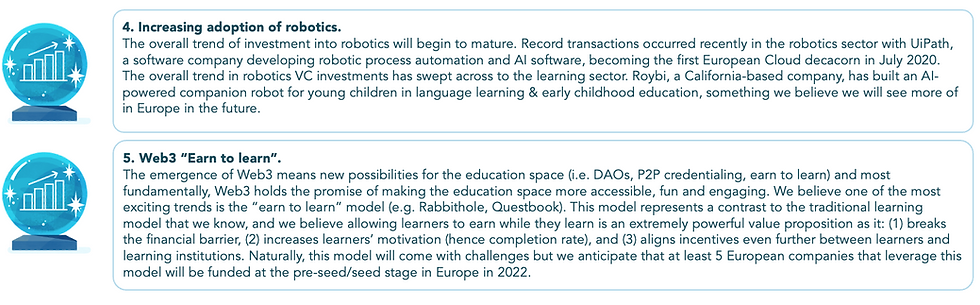

Our predictions for 2022:

Comments