The Half Year European Edtech Funding Report 2022

- The Brighteye Team

- Jul 14, 2022

- 2 min read

Updated: Dec 10, 2024

Following a barnstorming end to 2021, the Edtech sector, like many others, looked forward to continuing its momentum in 2022. However, the evolving financial and geopolitical environment has created highly uncertain investment conditions. Despite some promising signs of resilience, the global Edtech market has cooled, particularly in the earliest rounds. This said, European Edtech represents somewhat of an anomaly, with VC investment 40% higher in H1 2022 than at the equivalent point in 2021. This resilience, combined with the broader cooling in other markets, including the US, means that European Edtech VC now represents 22% of global Edtech VC, up from just 6% in 2020.

Headlines include:

1. Europe shows signs of resilience

While the global Edtech VC market cools, European Edtech VC is 40% higher than at the equivalent point in 2021, standing at $1.4B in 2022 compared to $1.0B.

2. Portion of global Edtech funding secured by European companies is increasing

In 2020, European Edtech VC represented 6% of global Edtech VC. In 2021, this portion grew to 11% and thus far in 2022, European Edtech VC represents 22%.

3. Deal sizes increasing, particularly in Europe

Average deal size in Europe in H1 2022 stands at $13.1M, compared to $8.4M in 2021. This represents investors doubling down on companies they consider robust and likely to be able to survive and thrive through the current environment.

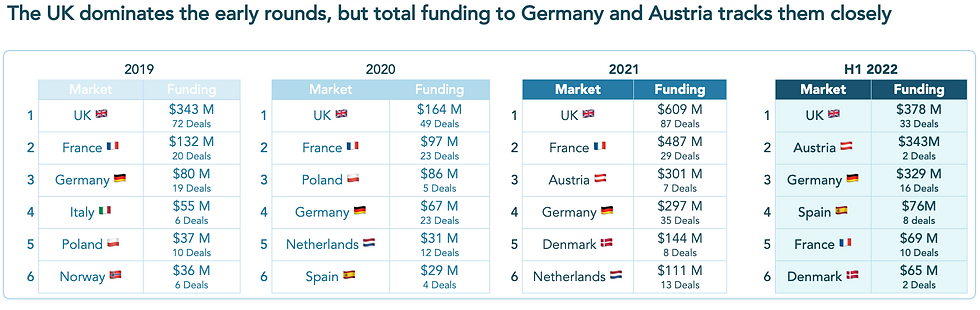

4. Increasingly robust European ecosystem, with the UK ahead on both funding and deal count

The UK retains the top spot it held at the end of 2021, with the highest funding total and the highest number of deals. Indeed, more than twice as many rounds have been raised by UK companies than in any other market. However, it’s worth noting that thus far in 2022, 3 of the top 10 largest rounds have been raised by Germany companies.

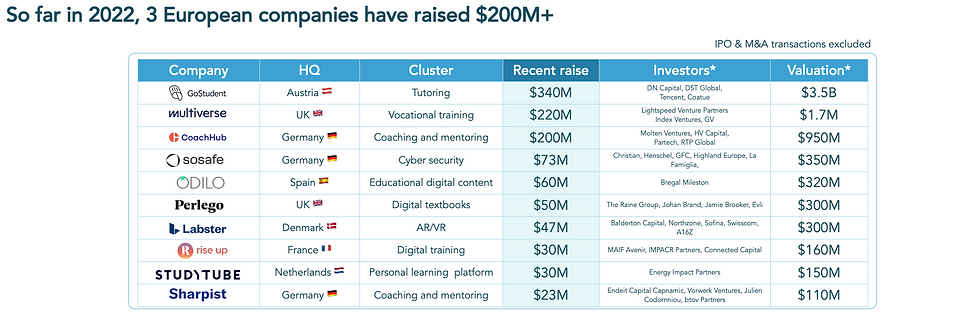

5. More than $200M raised by 3 European companies operating in 3 different verticals

In 2021, 2 companies raised rounds of >$200M compared to 3 thus far in 2022. This bodes well for the development of the ecosystem, as does the fact they cover varied verticals (early employment, tutoring and coaching).

Comments