Over the past 24 months, it has become increasingly clear to us that there are only two structural ways to address Europe's skills gap: either create the talent locally, or import it.

Across healthcare, construction, logistics and engineering, shortages persist. Demographics are not supportive. In many countries, the working-age population is shrinking while demand for skilled labour remains high, creating strong pressure on the labour market.

We have come across a number of companies rethinking how talent moves across borders and leveraging the strategic "talent importation" lever. At first glance, these businesses appear operational: visa support, relocation services, Employer of Record, compliance tools. However, we believe something structural is emerging in Europe.

In this piece, we share our thinking on:

- (a) Why we believe this space matters now

- (b) Our understanding of the early landscape (market map)

- (c) Where we believe the largest opportunities may lie

Disclaimer: Talent mobility (i.e. immigration) is a politically charged topic shaped by national policy, public opinion and ideology. In this piece, we do not attempt to address those debates. Our focus is narrower: the structural labour dynamics and the emerging infrastructure that enables cross-border talent mobility.

(a) Why we believe in this space

Our belief is driven by three structural trends that point to a long-term shift in Europe's labour market.

I. Europe's structural labour shortage

Europe faces persistent shortages across several essential sectors, and the gap is not evenly distributed.

Ageing is the underlying pressure. The EU population was estimated at 450.6 million in January 2025. People aged 65+ represent 22% of the population, up 2.9 percentage points over the past decade. The median age is 44.9, and the old-age dependency ratio stands at 34.5%, meaning just over three working-age people per person aged 65+. (source: Eurostat)

This demographic shift increases demand while reducing supply. More people require healthcare and long-term care, while more workers retire and fewer enter the workforce.

Healthcare is the clearest example. The EU faced an estimated shortage of around 1.2 million doctors, nurses and midwives as of 2022. The workforce itself is ageing: over a third of doctors and a quarter of nurses are aged over 55. (source: European Parliament)

Construction is another pressure point. In Q4 2024, the job vacancy rate in construction was 2.9% across the EU business economy, reflecting persistent unmet demand even as broader macro conditions fluctuate.

Similar constraints apply in logistics, manufacturing and care. Automation and AI may ease pressure at the margin over time, but they are unlikely to offset the demographic shift. The structural imbalance between labour supply and demand remains.

II. Cross-border work is becoming normal

Over the past five years, global employment infrastructure has improved significantly. Employer of Record platforms and global payroll providers such as Deel and Rippling have made it easier for companies to hire across borders without setting up local entities. International hiring is becoming more structured and repeatable.

There are also clear signals that cross-border labour mobility in Europe has normalised again post-Covid:

- Around 10 million working-age EU citizens (20-64) live in another EU Member State

- In 2023, 859,000 people moved to another country and 656,000 returned, a return to pre-pandemic levels

- Postings of workers (cross-border work arrangements) rose back to pre-pandemic levels, reaching 4.6 million

- Cross-border commuting has shown a slight upward trend to 1.8 million (around +8%)

(source: European Commission, Annual Report on Intra-EU Labour Mobility 2023)

However, the legal immigration process itself remains fragmented: visa categories differ by country, credential recognition is inconsistent and processing timelines vary. Much of the workflow remains manual and advisory-led.

This shift shows that the employment layer has modernised faster than the mobility layer. If labour markets are becoming more integrated, immigration cannot remain primarily manual and service-driven. There is a clear opportunity to integrate immigration directly into the employment stack and shift towards structured, automated workflows.

III. The increasing friction between mobility and skills

We see a logical convergence between talent creation (training) and talent mobility, especially at the European level. This is not a background observation: it is the central tension the market has not yet resolved. Today, training systems produce skills that are nationally certified. Mobility platforms move workers whose credentials may not be recognised at the destination. The two systems operate in parallel rather than as a connected pipeline. That gap creates friction that falls on the employer, the worker, and increasingly on public systems trying to fill shortages.

The friction today sits in the interface between skills and regulation. A large share of European labour markets is still shaped by regulated access to professions: the European Court of Auditors notes that the total number of regulated professions increased from around 5,400 (2016) to around 5,700 (2023), and varies widely by country. (source: European Court of Auditors)

That matters because importing talent at scale, especially with the growing number of regulated professions, without solving the following constraints creates friction:

- Credential recognition

- Work authorisation

- Visa pathways

- Ongoing compliance

Even within the EU, the recognition layer is not working smoothly. The European Court of Auditors estimates that the EU system for recognition of professional qualifications is used in only around 6% of intra-EU mobility cases, and highlights persistent issues such as limited electronic procedures and inconsistent application across Member States. (Source: European Court of Auditors)

Equally, it is difficult to build talent locally without considering portability. Skills increasingly operate in a global labour market. Employers compete internationally. Workers move across borders. The conclusion today is that work and talent operate internationally while regulation remains national. This misalignment creates structural friction for Europe and, at scale, that friction becomes an infrastructure problem.

We are convinced this is a one-way trend rather than a temporary shift. The IMF estimates that around two-thirds of jobs created in the EU between 2019 and 2023 were filled by non-EU citizens, suggesting that recent employment growth has been heavily migration-supported (source: IMF). In parallel, several essential systems are already dependent on internationally sourced workers: in the UK's NHS, 36% of doctors and 30% of nurses are non-UK nationals (source: UK Parliament), illustrating how cross-border talent has become embedded in workforce capacity. Even as macro conditions cooled, shortages remained visible in core sectors: Eurostat still reported a 2.9% job vacancy rate in construction in Q4 2024, and the European Labour Authority continues to flag transport and storage as facing substantial labour shortages across the EU. (source: Eurostat)

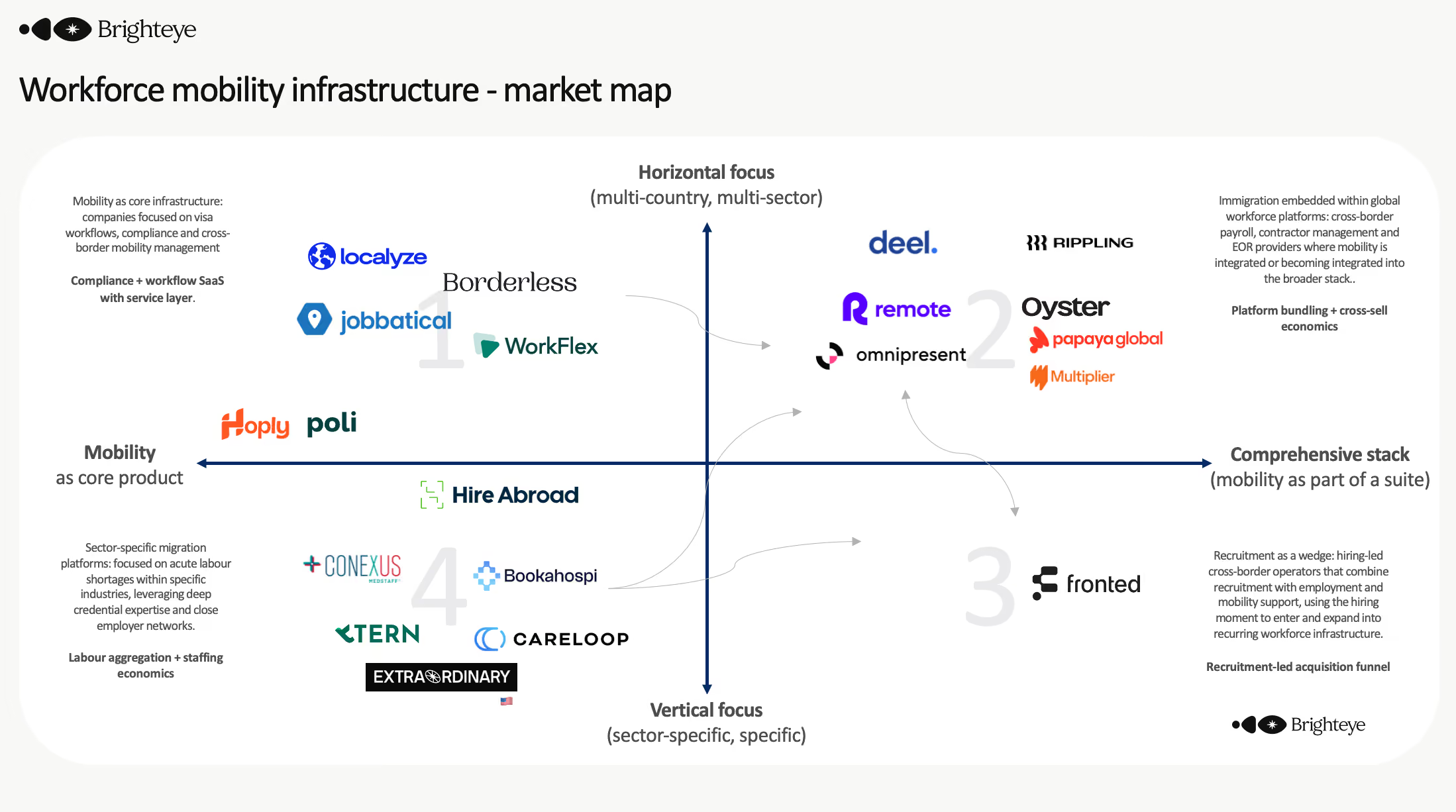

(b) Our understanding of the early landscape

Based on our research, we see four broad categories of players emerging in Europe.

1. Immigration-first platforms (quadrant 1)

These players focus directly on visa workflows and mobility management. Examples include Poli, Borderless, Jobbatical and other tech-enabled immigration providers.

Many are digitising case management and compliance tracking, though most remain partially service-intensive.

2. Global employment infrastructure platforms (quadrant 2)

These companies abstract payroll, contractor management and cross-border employment. Increasingly, they are expanding towards mobility. Examples include Deel, Remote, Rippling and Papaya.

Their strategic question is whether immigration becomes a feature within a broader workforce stack.

3. Recruitment-led cross-border operators (quadrant 3)

In this quadrant, recruitment acts as the entry point into recurring employment infrastructure, such as Fronted. This is strategically interesting because the hiring moment is high-intent.

4. Sector-specific mobility platforms (quadrant 4)

In sectors such as healthcare and engineering, specialised migration platforms are emerging. These players often combine credential verification with relocation and compliance support. Examples include Extraordinary.com (US), Tern, Bookahospi, Careloop. Vertical focus may allow deeper defensibility, although the addressable market is narrower.

Observations from the market map

Observation 1: The real control battle sits at the top of the map

The most intense competition is not between vertical specialists and horizontal platforms. It sits at the top of the map, between (a) immigration-native infrastructure builders, and (b) workforce platforms embedding immigration within a broader stack. The top quadrants compete for control of the mobility layer. The key question is whether immigration will be owned by infrastructure-native platforms, or absorbed as a feature inside larger workforce systems.

Observation 2: Immigration remains structurally service-heavy

Across all quadrants, operational intensity remains high. Even companies positioning themselves as tech-enabled still rely heavily on compliance expertise, local regulation knowledge and manual case management.

The category has not yet fully transitioned from advisory services to a talent operational infrastructure. The decisive shift will probably unlock automation depth and the ability to build structured compliance data layers that reduce marginal human input.

Observation 3: Europe's regulatory fragmentation creates space for a native control layer

Europe is structurally complex with 27 labour regimes, national visa systems and sector-specific credential rules. This increases operational friction, but it also increases the value of any platform that can standardise and automate that complexity across European Member States.

We believe long-term value in Europe will concentrate where immigration becomes core within the talent operational infrastructure built specifically for this regulatory fragmentation, rather than a peripheral module inside global payroll platforms.

Observation 4: Vertical migration remains underbuilt outside healthcare

Healthcare has attracted several sector-specific migration platforms such as Tern and Bookahospi. That makes sense given the scale and urgency of labour shortages in that sector.

However, other sectors - construction, manufacturing, logistics and skilled trades in Germany and the Netherlands - face similar structural gaps. We have not seen many tech-native, sector-specific mobility platforms emerging in these industries.

This raises an open question: is healthcare uniquely suited to vertical migration infrastructure, or is there an overlooked opportunity to build sector-specific mobility rails in other labour-constrained industries? If vertical migration expands beyond healthcare, quadrant 4 may not remain thin for long.

One underappreciated signal is the francophone engineering corridor. France holds a structural advantage in recruiting top engineering talent from francophone African markets, with limited competition from other European countries. The French "Carte Talent" visa - a four-year permit that also allows freelance consulting work - provides an accessible entry pathway. This is a concrete example of a corridor where the ingredients for vertical migration infrastructure are already present: a defined talent pool, a workable visa pathway, concentrated demand from French tech employers, and relatively low regulatory friction by European standards. It suggests that corridor-specific platforms, not just sector-specific ones, may be a viable entry point.

(c) Where we believe the opportunities may lie

We do not see talent mobility technology as a niche compliance tool but instead we see it as a missing layer in Europe's workforce infrastructure. Several opportunities stand out.

1. A full-stack mobility platform: from skills to relocation

This is the opportunity we find most compelling, and the one where we believe a genuinely new category could be built.

Today, mobility starts too late. Most platforms enter at the visa stage, after a candidate has already been identified and selected. That said, in many labour-constrained sectors, the bottleneck begins much earlier: skills, certification and employer alignment.

The bear case is clear: bundling training, mobility and employment into a single system is operationally complex, capital-intensive and requires excellence across very different disciplines. Most platforms have sensibly chosen to solve one layer at a time.

We think that is the right approach for now but not the right answer long-term. As Marius, the CEO of Fronted puts it: "A full-stack mobility platform is inevitable. In the long run, customer preferences win, and customers don't want to juggle multiple vendors just to make one hire. Every additional vendor increases friction and cost. Building and operating such a platform was previously out of reach, but AI makes it possible."

The opportunity is to build a platform that spans the entire lifecycle of a cross-border worker:

- Identification of talent in other markets

- Targeted training aligned to specific European employer demand

- Skills validation and exam preparation

- Work simulations and employer screening

- Conditional job offers

- Visa workflows and work authorisation

- Payroll and tax alignment

- Relocation logistics

- Onboarding and compliance monitoring

In this model, mobility does not begin with paperwork. It begins with talent pipeline creation. The platform would build private talent pools trained against real employer demand, then orchestrate the physical relocation and integration process end-to-end.

This is also where Brighteye's lens is most relevant. The convergence of learning and workforce mobility is not just a market observation, it is the architectural question at the centre of this space. Whoever connects skills creation to mobility infrastructure in a structured way will own a significant share of the labour supply chain for Europe's most acute shortages.

2. A European compliance engine

Europe does not lack immigration expertise. It lacks structured infrastructure to facilitate mobility at scale, both within and into Europe.

Immigration in Europe is fragmented, frequently updated and often discretionary. It is unlikely to become fully automated in the way payroll or payments have. Payroll rules are largely deterministic and standardised. Immigration rules are political, country-specific and sometimes subject to interpretation. That distinction matters: immigration may never become pure software. Human judgement and regulatory nuance will likely remain part of the process. This does not mean it cannot be systematised. The opportunity is not full automation, it is structured orchestration. Even if decisions remain discretionary, the surrounding layers can be standardised:

- Regulatory rule libraries

- Documentation logic

- Status tracking

- Employer obligations

- Ongoing compliance monitoring

There is also a distribution angle that is easy to underestimate. The visa processing relationship is one of the highest-trust moments in the employment lifecycle: a company hands over sensitive employee data, tight timelines and legal exposure. Platforms that handle this well earn a relationship that opens naturally into adjacent services: HR system integrations, payroll alignment, relocation logistics, and financial products for relocating workers. The compliance engine is not just a workflow product. It is a trust layer that, once embedded, is difficult to displace.

This also points to a structural integration opportunity. Immigration infrastructure can be delivered not only as a standalone platform but as an API layer embedded directly into ATS and HR systems, so that compliance workflows are triggered automatically at the point of hire. That positions the compliance engine closer to the employment stack rather than adjacent to it.

The question is whether a platform can reduce fragmentation enough to become the default compliance layer for cross-border employment, increasing predictability for companies and lowering marginal operational cost, even if lawyers and experts remain part of the loop.

As Kane, CEO at Poli, puts it: "There is real scope for technology to make a difference to such a fragmented and complex regulatory landscape. It is in Europe's best interests to reduce the friction associated with hiring and relocating top talent."

3. Vertical migration infrastructure (beyond healthcare)

Healthcare has attracted the most visible vertical migration platforms. That is not surprising. Shortages are acute, credentials are regulated and employer demand is concentrated.

The bear case for replicating this in other sectors is also real: construction is fragmented, manufacturing is localised and logistics is thin-margin. These characteristics make vertical infrastructure harder to scale and monetise, and help explain why tech-native platforms have not emerged here yet.

Our view is that the answer depends on sector structure. Vertical migration is viable at venture scale where three conditions are met: (1) regulated credentials that create a natural compliance workflow, (2) concentrated employer demand that allows structured sourcing, and (3) shortages severe enough to justify platform economics.

The open question is not whether these sectors have shortages (they do) but whether they can generate the workflow density and employer concentration that platform businesses require.

Concluding thoughts

Europe's labour markets are becoming cross-border. Regulation is not.

The gap between the two is widening, demographics are clear, labour shortages are measurable and yet immigration and compliance remain fragmented and largely service-driven.

We believe talent mobility is not a niche problem, it is a missing layer in Europe's workforce infrastructure.

The control point is still open and immigration may be absorbed as a feature inside global workforce platforms. Or it may evolve into a core, programmatic infrastructure layer built for Europe's regulatory complexity. That outcome is not yet decided.

There is also a broader strategic frame worth naming. The competition for global talent is no longer just a business problem. It is a geopolitical one. The US has long benefited from concentrating the world's best engineers and researchers. The Gulf states are now actively building infrastructure to do the same. Europe has world-class universities, a large diaspora of internationally mobile workers, and structural demand across every major sector. What it lacks is the infrastructure to convert that potential into organised talent flows. The founders building in this space are not just solving a compliance problem, they are building the rails that will determine where the next generation of global talent lands.

For founders building in immigration infrastructure, full-stack mobility or sector-specific migration rails, we would like to speak. We are particularly interested in teams aiming to build durable infrastructure, not just workflow tools. If you are working on this, reach out (dg@brighteyevc.com).

Thank you to the following founders for their insights and great feedback: Marius (Fronted), Matt (Borderless), Kane (Poli) and Mo (Extraordinary.com).