VC funding secured by European Learning & Work companies more than doubled from 2024 to 2025 and the number of deals jumped 21%. Global funding also increased but less significantly than in Europe.

While conventional Edtech funding levels remain below the peaks we observed in 2021, innovation and capital are increasingly converging around a broader learning & work stack, extending beyond education delivery into skills activation, productivity, hiring, and mobility.

Hence, this report has become the ‘Learning & Work’ funding report.

To this end, within this year’s report and in addition to the headline funding and activity data, we consider two different ways to understand the Learning & Work space.

The first considers three sub-categories in the sector that follow its evolution in recent years: conventional Edtech (K12, Higher Education, lifelong learning); corporate and workplace learning; and productivity and talent platforms.

The second considers a ‘value chain for learning & work’, working through 'learn' (foundational knowledge), 'place' (contextualising skills within work), 'perform' (on-the-job effectiveness, productivity) and progress (career mapping, uskilling and skill portability). This is more focused on the ‘purpose’ of specific solutions rather than their user base.

What follows here is a summary of some of the key takeaways.

For the full report, you can download it below:

Discover the full report here!

1. European learning & work VC funding more than doubled from 2024 to 2025

European VC funding into companies in the learning & work space surged from 2024-2025, more than doubling from €710M to €1.6B. This matches the highest funding total since the highs of 2021. Global VC funding’s resurgence was impressive but slightly less emphatic, with an increase from €5.4B to €9.0B. Deal count also surged, with European deal activity being its highest since 2018 – the same was true of global deal activity, with 1400 deals being the highest deal tally since the 1403 recorded in 2018.

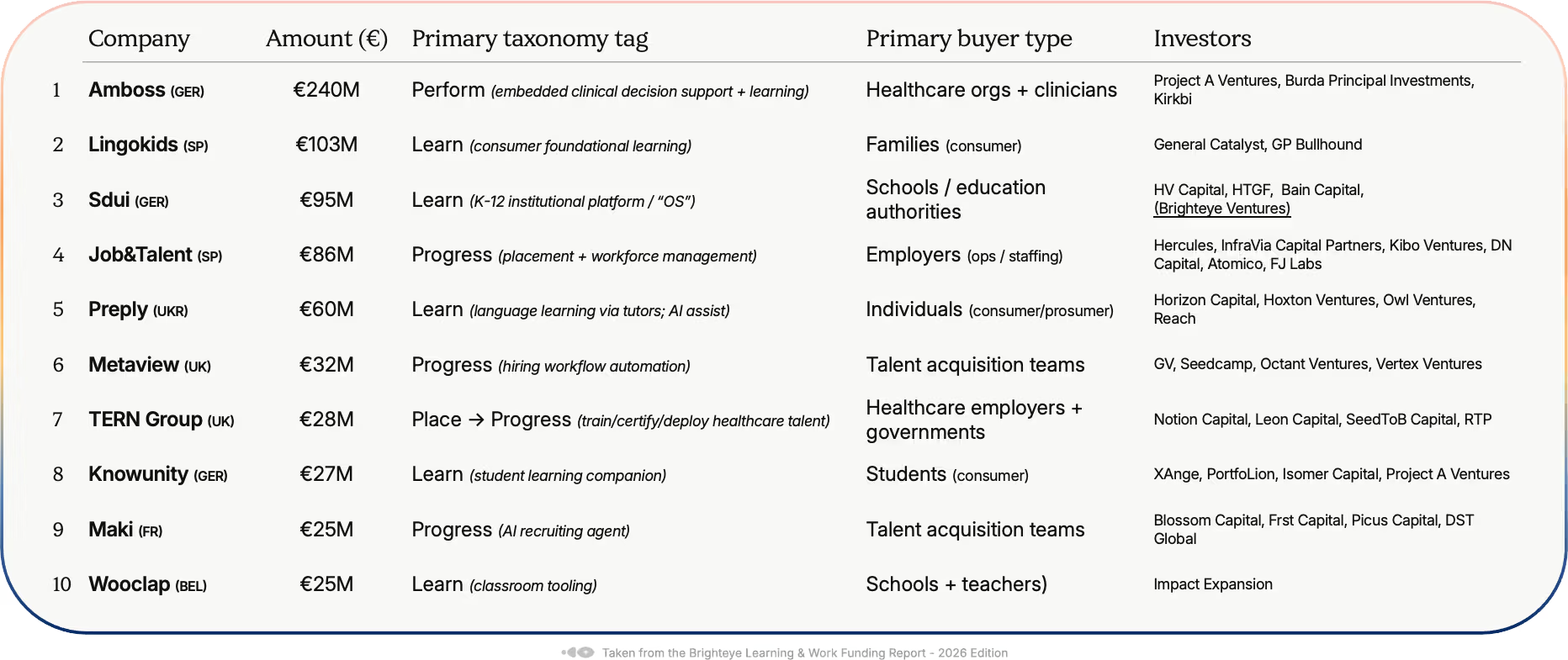

2. The biggest cheques in Europe are secured by companies in regulated markets and those operating within institutional procurement processes

The top of the market is highly concentrated and top-heavy. The top 3 rounds (Amboss, Lingokids and Sdui) sum to €438M, which is ~61% of the top-10 total (€721M). This suggests Europe’s headline funding story is being driven by a small number of “winner” raises rather than broad-based mega-round depth.

Big cheques are going to businesses with clear monetisation rails: regulated enterprise, institutional procurement, or high-frequency operational ROI. In the top 10, we observe (i) healthcare workflow/decision support (high-stakes, sticky), (ii) K-12 infrastructure (procurement + embedded), and (iii) staffing/hiring systems (directly tied to cost). In contrast, pure “nice-to-have” productivity or engagement tools don’t appear in the top 10.

Two dominant growth engines show up in the top 10 deals: consumer scale brands and “automation of labour-market transactions.” Lingokids + Preply + Knowunity reflect consumer distribution and repeat usage; Job&Talent + Metaview + Maki reflect digitising and automating the hiring/placement pipeline.

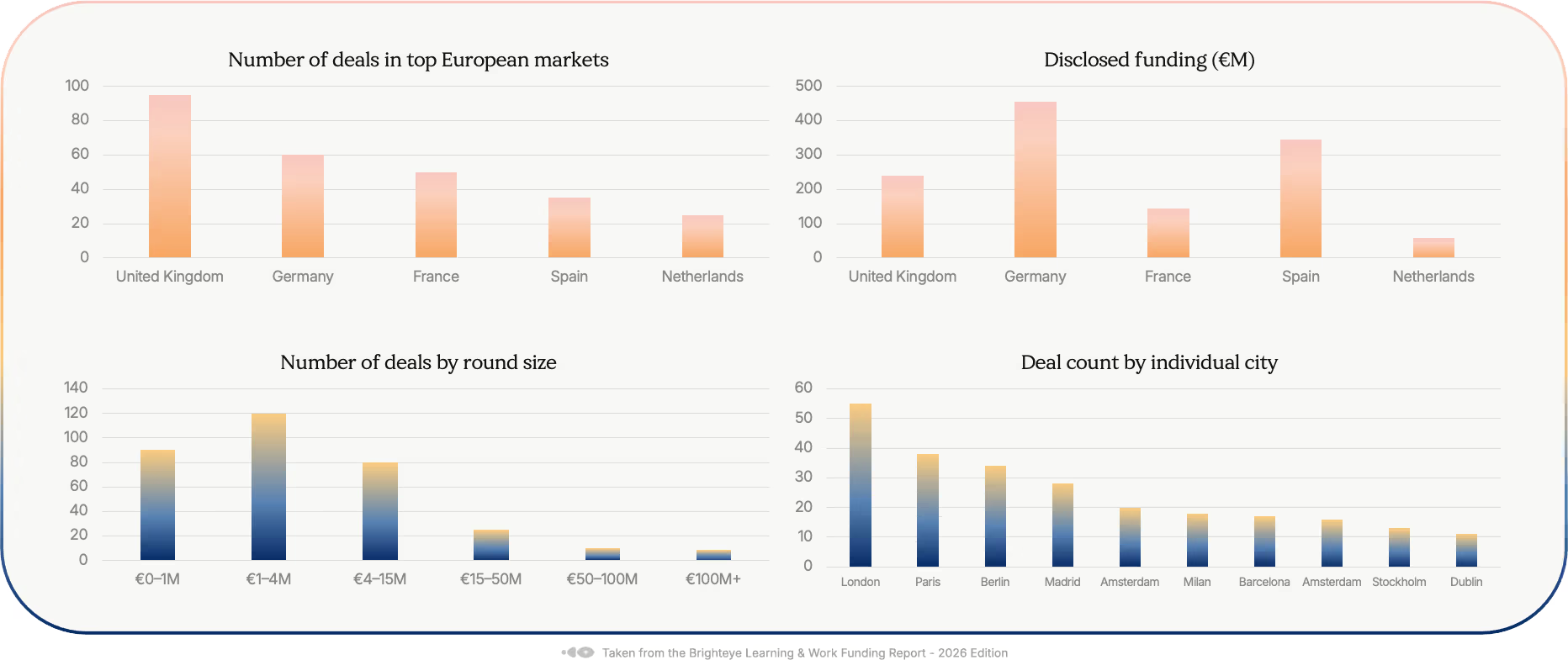

3. The UK, Germany, France, Spain and the Netherlands, together account for over 80% of deals

Europe’s Learning & Work funding landscape is dominated by five hubs: the UK, Germany, France, Spain and the Netherlands, together accounting for over 80% of deals and an even higher portion of all disclosed capital. Disclosure rates vary sharply by market: the UK shows the highest transparency, while Germany and the Netherlands skew heavily toward undisclosed early-stage rounds - reinforcing the view that Europe’s pipeline is widening at the bottom of the funnel.

Capital concentration remains city-led rather than country-led, with London, Paris, Berlin and Madrid acting as continental gravity wells for both talent and capital. Notably, Milan and Dublin are seeing increases in learning & work deal activity.

4. The most active learning & work investor globally in 2025 was Y Combinator

Europe’s capital stack is front-loaded with public and quasi-public investors playing an outsized role in sustaining early experimentation; this naturally supports deal volume but may dampen late-stage capital intensity and valuation velocity.

Sector specialists appear earlier and more selectively in Europe. Often anchoring conviction at Series A rather than leading volume at seed; globally, specialists drive category consolidation and capital clustering.

Looking to the global data, we’ve written previously about the increasing frequency of Y Combinator having explicit learning & work themes in their calls for startups. It's therefore not surprising to see them sat on top of the global activity rankings. Also of note, we see hugely successful generalists taking a bigger interest in the sector, including General Catalyst, Andreesseen Horowitz, and Sequoia.

As referenced in the introduction, we broke down the space into three well-understood clusters to give a sense of respective deal and funding density.

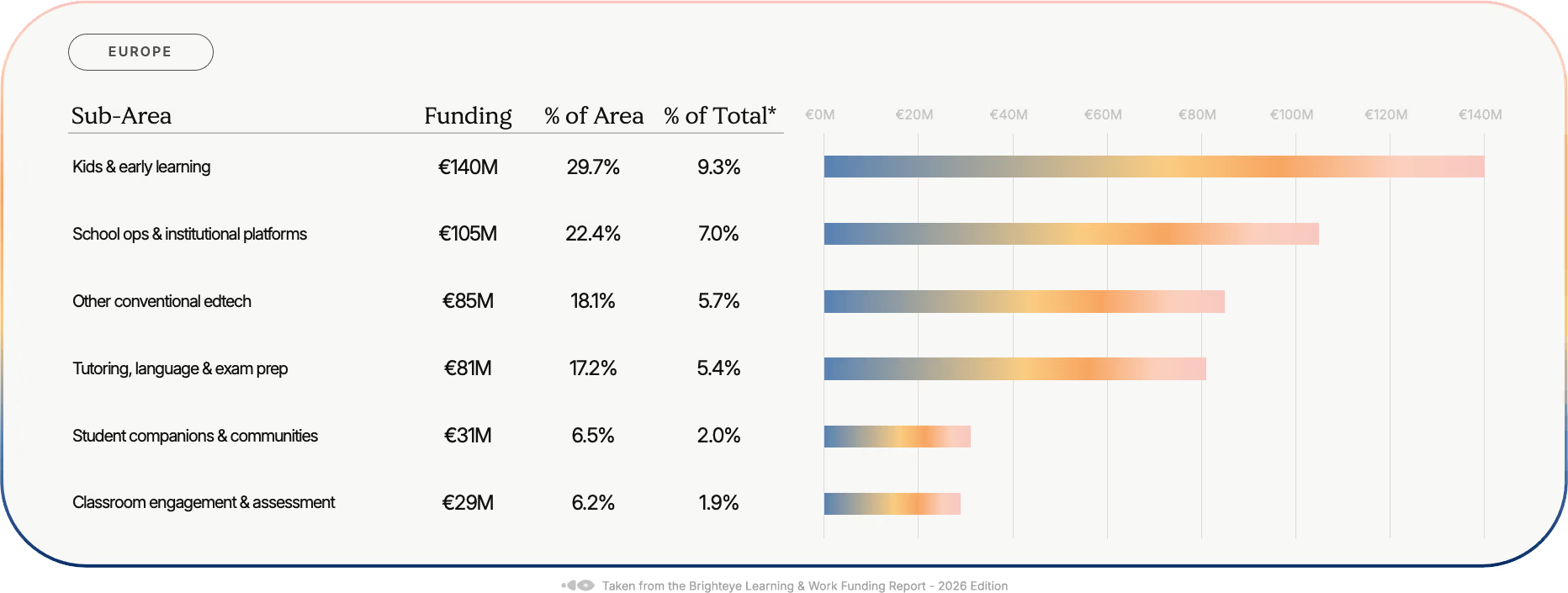

5. Conventional Edtech covering K12, HE and lifelong learning

Conventional Edtech remains the bedrock of the category, particularly in Europe where public education systems, regulation, and procurement cycles shape market dynamics. Companies in this space raised €471M in 2025.

This segment includes:

- K-12 platforms (digital classrooms, tutoring, assessment tools)

- Higher education technologies (LMS, student engagement, credential management)

- Lifelong learning platforms aimed at individuals rather than enterprises

These companies tend to operate in institution-centric markets, where buyers are schools, universities, or public bodies.

6. Corporate and workplace learning

Represents the most significant expansion of the Edtech category over the past several years and one of the clearest links to future-of-work investment themes. Companies in this space raised €601M in 2025.

This segment includes:

- Enterprise LMSand LXP platforms

- Upskilling and reskilling providers aligned to job roles

- Skill intelligence and workforce analytics tools

Crucially, corporate learning platforms are being evaluated less as content providers and more as decision-support systems for organisations managing human capital.

Here, the buyer shifts from schools and universities to employers, and the value proposition shifts from learning completion to learning impact.

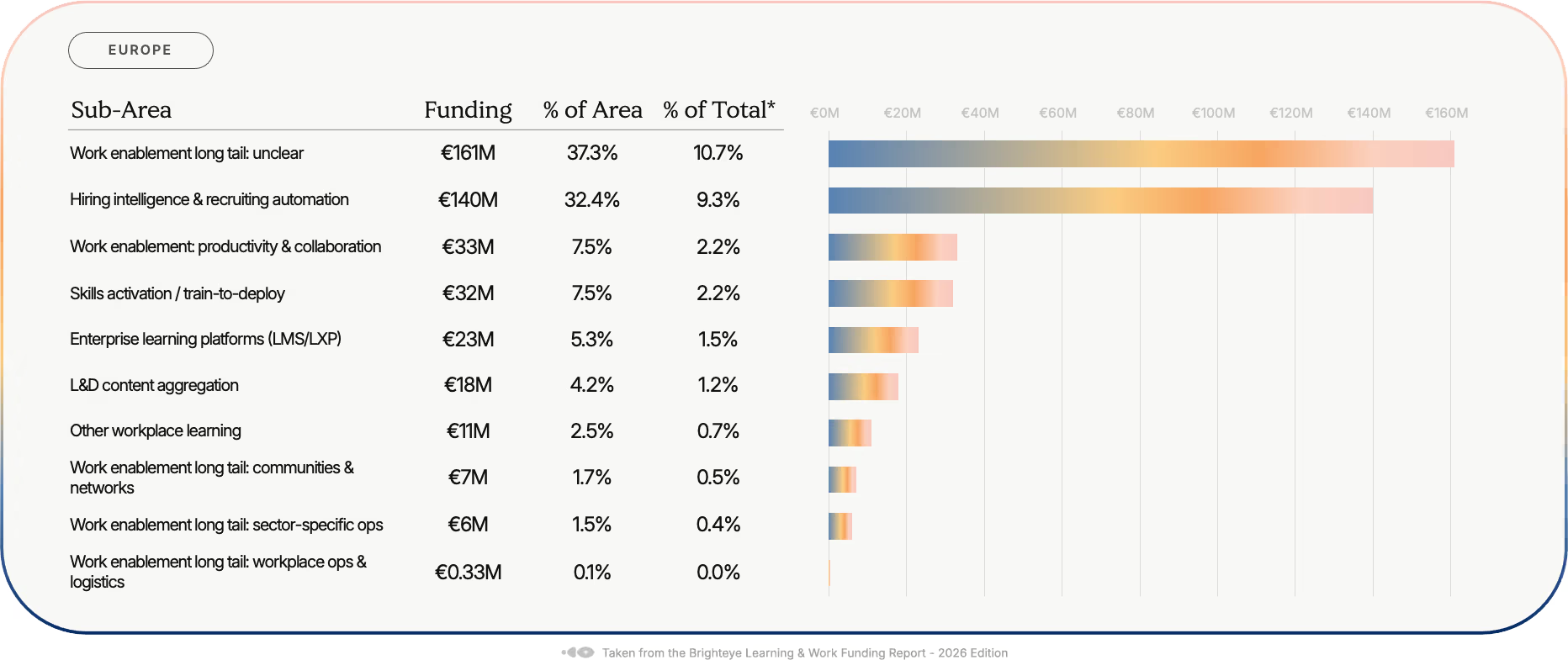

7. Productivity and talent platforms

The most forward-leaning part of the ecosystem sits at the intersection of learning, productivity, and performance. These platforms do not position themselves primarily as “learning tools” at all.

Instead, they aim to:

- Reduce friction in task execution

- Provide real-time guidance or augmentation

- Improve performance as work is happening

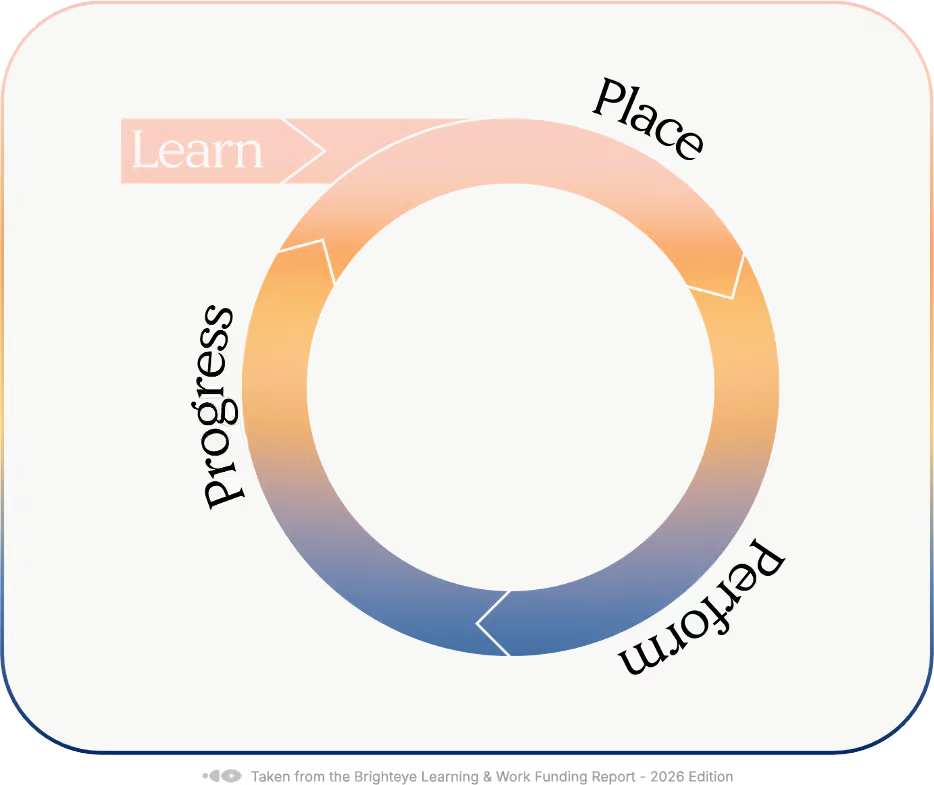

8. An alternative taxonomy: the value chain for learning & work

Understanding the learning & work space through the three core buckets of i) Conventional Edtech, ii) Corporate and workplace learning and iii) Productivity and talent platforms, provides a helpful lens through which to understand the space.

But, getting underneath the purposes of each of the three buckets provides a complementary perspective on how solutions interface one another.

Learn: We suggest thinking about this section as foundational knowledge – developing core capabilities that will drive learning outcomes that support a person’s entry into the labour market. It would therefore include K12, Higher Education and Vocational Education, alongside other core skills formation.

Place: We suggest thinking about this section as applying knowledge and skills within a relevant context. ’Place’ refers to finding a home for said knowledge and skills. This includes some but not all early talent marketplaces.

Perform: This can be interpreted as executing and improving performance in a role – it can also be interpreted as productivity and outcome-enhancing.

Progress: We suggest interpreting ‘progress’ as supporting individuals’ career trajectory and advancement, both within and between careers, hence the reference to portability in this section.

We break down 2025 activity into these clusters in the report. We will be revisiting this framework in the coming weeks!

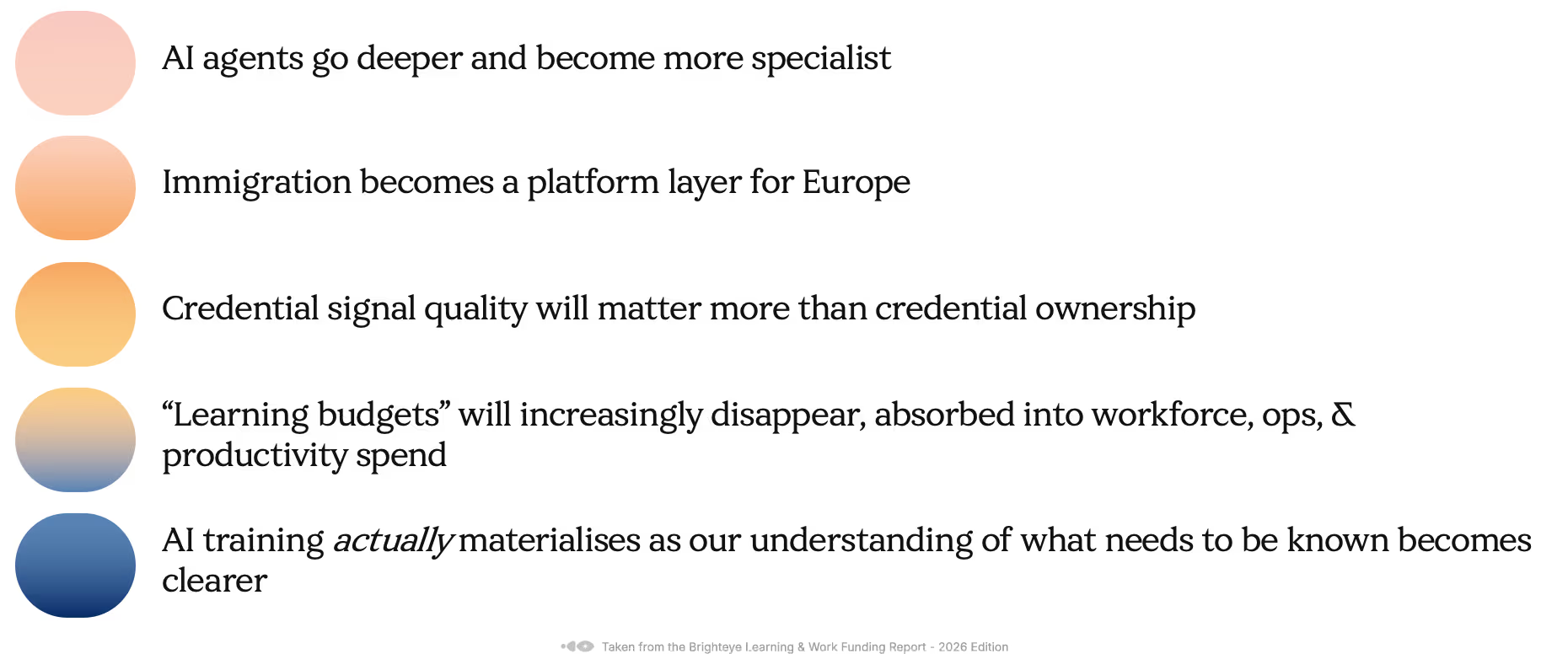

Predictions for 2026

Within the report, we reviewed our predictions for 2025 and also put forth some predictions for 2026, harvested from across the Brighteye team. We get underneath each of these predictions with a brief, specific prediction on the levels of deal activity we expect in the year.

We hope you enjoy the report.

Discover the full report here!